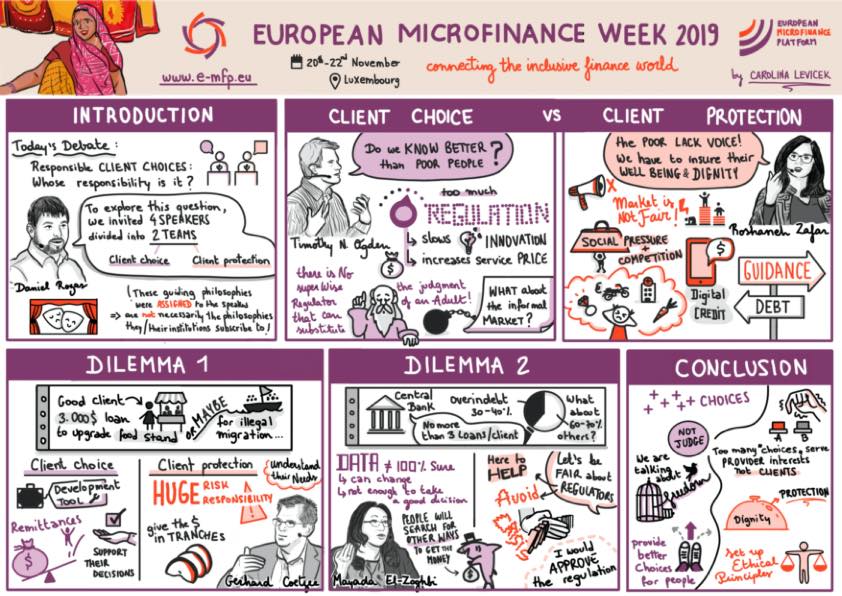

Plenary: Responsible client choices in finance: Whose responsibility is it?

- Daniel ROZAS, European Microfinance Platform (e-MFP)

- Mayada EL-ZOGHBI, CFI at Accion

- Gerhard COETZEE, CGAP

- Timothy N OGDEN, Financial Access Initiative

- Roshaneh ZAFAR, Kashf Foundation (Pakistan)

DISCUSSION

Daniel ROZAS introduced the closing plenary by highlighting the challenges that MFIs, investors and regulators have in reaching a balance between client choice and client protection in their daily work. He argued that too much client protection may limit the client’s autonomy, while too little may lead clients to make wrong choices.

To illustrate the difficult decisions that practitioners have towards their clients, the panellists were divided into 2 groups: Timothy N. OGDEN and Mayada EL-ZOGHBI advocated for client protection, while Roshaneh ZAFAR and Gerhard COETZEE defended client choice. Rozas emphasised that the opinions presented during this plenary were fictitious and purposely divergent, and not necessarily those held by the presenters. Rozas then explained the structure of the debate: each team would have the opportunity to present their opening statements, ask questions to each other and respond to pre-formulated dilemmas. The audience then voted for one of the groups, based on the credibility of their arguments.

Ogden started off by presenting the views of the client choice group. He reminded the audience of the early days of microfinance, and argued that the sector could only develop because it was not strangled by regulators. He also suggested that it took microfinance actors 30 years to figure out the deep embeddedness of the financial lives of clients, and how products could serve them best. He then questioned how severely capacity-constrained regulators could ever understand the needs of the sector and make decisions on behalf of clients. In this line of thinking, Ogden argued that, if we started implementing more regulatory constraints in microfinance, this would raise costs for MFIs. As a result, customers would end up paying that cost and resorting to the informal market, served with very low-quality products.

Roshaneh Zafar’s opening statement for the client protection group revolved around the story of a vegetable trader called Sabina, a microfinance client faced with several social pressures and with the need to invest in her growing business. The statement was continued by Gerhard Coetzee, who explained that the story described by Zafar is the reality of the majority of microfinance clients. He argued that, without leadership and guidance, Sabina would take multiple loans, from many different organisations, in order to deal with the social pressures she is faced with. Coetzee explained that clients prioritise short-term needs, competing with long-term opportunities. He then defended that this puts such clients at risk of losing their assets and future.

Zafar complemented that client protection is about ensuring the dignity of clients. She elaborated that the odds are heavily against the poor, and that we are currently pushing credit into clients with limited choices. To exemplify this, Coetzee shared that, in Kenya, 30% of people are behind with their digital credit loan payment, which is a reality resulting from bad client choices.

Following the opening statements, Ogden was invited to pose a question to the client protection group. He questioned his opponents on which major financial decisions in their lives they would entrust to a regulator. Zafar answered that clients should be at the centre of the debate; once regulators are more attuned with the needs of clients, they can guide them best.

Zafar then addressed the unequal access of women to financial services, and how the opposing group would suggest to create a level-playing field. Mayada El-Zoghbi acknowledged that the market is not fair, but that the role of microfinance stakeholders is to empower them. She further elaborated that it is not our role to pre-empt clients’ decisions, but to provide clients with tools to make good choices.

DILEMMAS

The first dilemma posed by Rozas to the panellists revolved around a microfinance client who runs a food stand, but whose husband and son are planning to migrate illegally to a wealthy country. As a loan supervisor, the two different groups were asked to think about their obligations, and whether to trust the client in making the right decision.

From the client protection perspective, Zafar revealed that she herself worked as a loan officer for 3 years, and this is indeed a real-life story of an economic migrant. Zafar then argued that illegal migration represents both reputational and moral risks for the lender as it is replete with huge risks to the client and her family and the returns are highly unpredictable. It is thus the responsibility of the loan supervisor to conduct a credit appraisal, assess the potential of this client’s business in order to meet the demand for credit, and find other opportunities within the household for this family to get credit.

On the client choice side, El-Zoghbi defended that the mission of an MFI is to take decisions which are good for its clients. She explained that migration is an investment that can give this family long-term returns, and can be much more significant than a food stand. El-Zoghbi further argued that remittances have a direct link to poverty reduction. She acknowledged that there is risk in everything we do, and that the risk intrinsic to illegal migration has to be treated like any other risk.

The second dilemma revolved around the head of supervision at the central bank who has to approve a draft regulation prohibiting more than 3 loans per client. The bank commissioned research that revealed that among clients with more than 3 loans, about 30-40% have high rates of overindebtedness, but the remainder have no difficulty making repayments and have put these loans to good use. The dilemma herewith was whether to approve the new regulations or leave it to clients and institutions to decide.

Ogden answered that regulators cannot know the details which are most important for the client’s decision. He further defended that the mentioned regulation would substitute our judgement on people that are doing fine, and that imposing such limitations would lead those who needed to borrow to take loans from the informal market, not stop them from borrowing—and that would ultimately be much worse for the customer.

Coetzee then argued that regulators have traditionally allowed the microfinance sector to develop, and can still play a role in helping the market grow. Regarding the specific dilemma, Coetzee suggested that the problem does not lie on the number of loans, but on the loan amounts. He defended that service providers should be required to report on customer outcomes.

In the closing statements of the client protection group, Coetzee acknowledged that choice is important, but emphasised that most choices are used to entice people into solutions that add no value to them. He added that most business models around the world exploit choice. Zafar complemented that we should strive towards bringing benefit to the client.

On behalf of the client choice group, El-Zoghbi argued that the industry failed to make better choices for people, and this has been the entire premise of the development field. She further defended that development is about increasing the number of choices and empowering people to make these choices. El-Zoghbi also argued that we do not understand and have no right to judge people’s trade-offs, and that we should increase choices and give people their own tools to make the right choices.

The audience vote showed a close score between the client protection and the customer choice teams.